Gross Financing Needs is a Weird Indicator - Part 1

Why does it have to be so weird...

The IMF’s debt sustainability analysis (DSA) for Sri Lanka has a whole bunch of questions. Theo Maret and Brad Setser had explored this in an excellent piece recently as well. A specific point within this was on the IMF’s Gross Financing Needs (GFN) indicator - an indicator I share some (relatively) strong thoughts on. In this piece, I’m going over GFN and issues with a focus on it, and in a follow-up piece I’ll use Sri Lanka’s example to illustrate additional complexities.

What is GFN?

I won’t go into the origins of GFN as an indicator (though I think there is merit in exploring whether corporate quarterly cashflow projections are a relevant methodology for long-term sovereign financing requirements). Instead, let’s look at what it is, and how there are plenty of issues with it.

Gross Financing Needs effectively refers to all the financing requirements a sovereign has within a given time period. This includes fiscal deficits (including interest payments due) as well as debt amortizations. One way to think of this is how much money is needed to be raised to meet the payments due in a particular year. GFN is often given as a % of GDP, and the IMF used to have a 15% of GDP benchmark for GFN, though this is now more context-specific. In any case, what GFN is quite straightforward. However, projecting this can create significant issues.

Tenors matter for GFN - when will the new cashflows come due?

A key issue with GFN projections is that it requires projecting what future cashflow needs would be. For deficits, this is somewhat straightforward, if you can project revenue and expenses, you can get a good enough idea (excluding interest for now). However, when you take debt that is due, a key issue is how you refinance it and at what tenor.

To illustrate this, let’s take an example where a country (let’s call it GFNland) has USD 100 of debt maturing in 2023, revenue and non-interest expenditure balances off (primary balance), and has a GDP of USD 1000. Let’s project that the primary balance remains in balance and GDP grows at 2% annually.

When looking at the GFN for GFNland in the future, you now have to decide what to do with the USD 100 maturing in 2023.

Let’s take 2 examples to show the divergent GFN that can exist.

In Option A, the USD 100 is refinanced as a 5% interest 12-month T-bill that is refinanced similarly every year.

In Option B, the USD 100 is refinanced through a 5% coupon 5-year T-bond that is refinanced similarly when it’s due.

The following graph shows the GFN as a % of GDP for the 2 options.

Just this single assumption makes two widely different GFNs. If you take Option A, the country maintains GFN that is slowly rising across the 10-year period we’re looking at. This is a completely different message from Option B, where GFN is low in between, and spikes in the years that the principal is due, but at the end of the 10 years is actually LOWER than starting out.

Reinvestments of reinvestments - how are those accounted for?

But what about the reinvestment of the coupon? Doesn’t that cause the GFN to rise too? Good question! But the complexity still exists.

Let’s take 2 more options -

In Option C, the coupon is reinvested in a 5% interest 12-month T-bill

In Option D, the coupon is reinvested in a 5% coupon 12-month T-bill and rolled over, but every 5 years, that T-bill is reinvested into a 5-year bond.

Once again, these two options give two significantly different GFNs. in one, the GFN falls from 2028 to 2032, while in the other it’s an increase. All of these have changed so much based on the reinvestment and tenor assumptions, and this matters.

Inflation and interest rates can have large impacts on GFN

Beyond this, there are other factors that matter significantly. In my view, the two most important are what we assume future interest rates are and what we assume future inflation is. Interest rates matter because they directly affect the reinvestments and what rate the reinvestments happen at. Inflation matters because GFN as a % of GDP is against nominal GDP - so rising inflation affects the denominator.

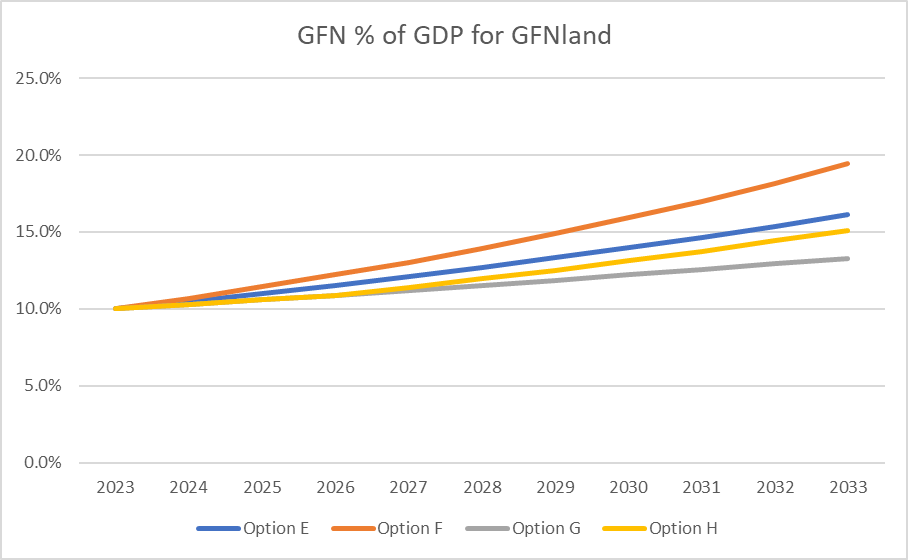

To illustrate this, let’s take 4 scenarios for just the 12-month T-bill option.

In Option E, the interest rates are at 7%

In Option F, the interest rates are at 9%

In Option G, the interest rates are at 7%, but there is 2% higher inflation per year

In Option H, the interest rates are at 9%, but there is 4% higher inflation for 3 years, before returning to 2% inflation

Since we’re using only the 12-month T-bill, it’s not as divergent as if we used different instruments, but as you can see, there are still significant divergences among the trajectories. If you add varied instruments, tenors, and reinvestments into the mix, these differences become compounded with the interest rate/inflation issues.

So why use GFN at all if it’s so inaccurate?

In reality, things are even more complex since different instruments have different rates and different reinvestment needs. The simple answer is this - getting an accurate indicator of GFN is not realistic. Whatever you choose to do involves taking many assumptions upon assumptions upon assumptions, and the likelihood of getting all of this right is so low it’s almost impossible.

My view is that it shouldn’t be used as a priority indicator. GFN projections still have their uses in seeing where payments can bunch up, and how changes in different factors like inflation, rates, and tenor management can affect government financing needs. However, these aren’t accurate indications and should be treated as such. These are only useful indications, not correct ones.

Trying to get precision into GFN targets can lead to inaccurate understandings of the future. A great example of this is Sri Lanka itself - what Sri Lanka’s ACTUAL GFN looked like in the past compared to the IMF’s past 15% benchmark. GFN ALWAYS did worse than the benchmark, and a big reason was due to the fact that reinvestments of reinvestments can’t be accurately included within this indicator.

Using GFN as a priority indicator can create issues - such as for Sri Lanka where the GFN target is a key part of the country’s DSA. Thankfully, the restructuring of the domestic bonds likely had a marginal impact on the actual long-term value of the bonds, but in a context where the impact HADN’T been marginal, it would have been done for an inaccurate and likely impossible to be an accurate indicator.

Of course, countries like Sri Lanka that have little ability to change the global sovereign debt architecture on their own (though precedents from Sri Lanka obviously matter) can’t unilaterally challenge and refuse to accept the IMF, and would likely have to go along anyway. But could there be better approaches from the IMF in the future? I think so. To me, GFN is at best a weird indicator that is useful to fiddle around with to see different scenarios, and at worst a complicated overly metricized mess. It shouldn’t be the basis of what determines a country’s future in my view.

I will end this piece with a short quote from Theo and Brad’s piece on this that excellently encapsulates their advice to the IMF on this, and follow up later with more specific issues with GFN from a Sri Lankan context including how the CBSL T-bills reprofile, the 0.5% of GDP reduction from T-bonds, and local inflation and interest rates affect the DSA through the impacts on GFN.

“Complex models should not trump common sense”