How much external debt repayments does Sri Lanka have to make in 2025?

Now that Debt Restructuring is (almost) complete

In December 2024 Sri Lanka announced completion of almost all of its International Sovereign Bonds (ISBs) which was last major milestone to complete its external debt restructuring process. There are a few things left to be done such as the ISB portions held by the controversial Hamilton Reserve Bank, the govt guaranteed Sri Lanka Airlines Eurobond, and finalization details with a few minor bilateral lenders as noted in a recent Ministry of Finance (MoF) document.

Given all this, there ought to be a good understanding of the foreign debt repayments that Sri Lanka’s public sector has to handle in the years ahead. But the public data that is readily available is not that forthcoming, requiring us to dig into some nooks to get a better picture. There are a few nooks I looking into in this article, CBSL Pre-determined FX net drains data, MoF documents, and right to information requests to the External Resources Department (ERD). Hopefully, CBSL or MoF will provide more clarity on this in their upcoming annual reports or in the upcoming Budget documents. But for now this is what I have at hand.

Using & interpreting CBSL Pre-determined Net FX drains data

That’s a mouthful of words for the dataset and the nuances involved with using the data can be longer than that. This Pre-determined Net Drains data is found alongside the rest of the monthly reserves data release of the CBSL and is a requirement under the IMF data disclosure standards that Sri Lanka seems to be part of since around 2013 - which is as far back as this dataset goes. Sri Lanka only reports outflows data and not inflows data. The purpose of this data is to provide a picture of the FX outflows that might require use of the FX reserves. It is provided as outflows for the next 12 months, with a breakdown for next 1 month, 2nd to 3rd month, and next 9 months.

The pre-determined data is provided in three parts. The first covers FX flows pertaining to Foreign currency loans, securities, and deposits, which covers the conventional foreign debt including ISBs and IMF loans. The second covers FX flows pertaining to forward and futures in foreign currencies vis-a-vis the local currency (this is where swaps taken by CBSL are covered). The third covers other FX liabilities like repos. The first two are the significant ones. The third one is negligible, other than during Sept 2020 to Feb 2021 when $1bn in US Treasuries were repoed to the US Federal Reserve to obtain liquidity during the US Treasury market volatility.

Pre-determined Net FX drains pertaining to Foreign currency loans, securities, and deposits

Figure: Pre-determined FX Debt repayments for next 12 months at end of each month, $ million

As you can see from the chart, Sri Lanka faced substantial FX outflows through the 2014 to 2022 period, rising from just above $4bn in 2014 to almost $7bn in 2022. After the external debt default in April 2022, you can see the drop in FX debt repayment obligations. There was a second fall in FX debt repayments obligations in October 2023 when the Asian Clearing Union (ACU) debt was restructured away into a swap with the RBI. The chart also shows a clear rise in repayment obligations over the next 12 months in Dec 2024 with the completion of debt restructuring.

Figure: Pre-determined FX Debt Repayments in next 12 months in Principal & Interest, $ million

The FX reserves to FX debt repayments ratio can be a useful ratio to understand whether Sri Lanka’s reserves are adequate and was even used as a condition in the usability of the PBOC’s RMB 10 billion swap. When the ratio is above 1.0, it means that reserves are larger than the outflow obligations in the next 12 months - indicating space to handle those obligations through reserves. While for most of the time CBSL has managed to keep this ratio above 1.0, during the 2021-2022 period the ratio fell below that and even into negative territory underscoring the crisis faced by early 2022. At end-March 2022, pre-determined FX outflow obligations were $7.1bn against reserves of just $1.9bn (which included around $1.5bn in the then unusable PBOC swap). Since 2023, the reserves buildup has helped improve the reserves to FX repayments ratio significantly, but with the increased repayment obligations post debt restructuring the ratio declined a bit in Dec 2024.

Figure: Pre-determined FX Debt repayments to Gross Official Reserves, $ million & ratio

What’s not covered in the Pre-determined FX debt outflows?

However, the pre-determined outflows data does not cover all the potential FX debt outflows that Sri Lanka has to finance. It only covers the FX liability related outflows to be handled by the central government and CBSL, meaning that outflows related to the banking system, SOEs and private firms do not feature in it. While the central govt and CBSL accounts for over 90% of such outflows, it does not cover the totality.

Its not all about external debt repayments alone

In the past when Sri Lanka Development Bonds (SLDBs) were still around, the FX repayments pertaining to those also appeared to be included within the predetermined outflows, since it is an FX liability of the central government and if unable to source FX for their repayments from elsewhere the government might have purchase FX from the CBSL reserves for that. In the data for 2022 at end-2021, the size of the SLDB related outflows were probably as much as $1.5 billion of the $7 billion in outflows from conventional FX debt.

Another aspect covered within the data are payments related to the Asian Clearing Union (ACU), which allows netted repayments on trade with regional countries every 2 months. Every two months the CBSL has an FX repayment to handle which is included in the pre-determined data. Usually this is about $200-500 million, every 2 months (Jan, Mar, May, Jul, Sept, Nov). However, during 2022 the ACU debt was not repaid and instead accumulated up to $2bn, keeping the pre-determined FX outflows elevated until late-2023 despite the sovereign default reducing other repayments. As mentioned earlier, this was only removed after Oct 2023 when the ACU debt was restructured away into an RBI swap.

This has meant that the pre-determined outflows data relevant to principal and interest payments of loans and debt securities could not be taken to be entirely repayments related to external debt related to bilateral, multilateral and commercial debt. Some amounts of domestic FX debt and trade related payments were also covered within it.

Pre-determined FX Net Drains pertaining to Swap and others

These are covered separately as short and long positions relative to the domestic currency. Short positions relate to FX borrowed by CBSL and Long positions relate to FX lent to others. Long positions have been small and rarer, with $200-350mn during 2021-2023 being the most prominent. Short-positions have been there consistently, ranging from around $500mn to $3.5bn. The net short position as a result has varied over time, from peaks of around $3.5bn in mid-2015 and 2024.

Figure: Pre-determined Net Short Position of CBSL over next 12 months, $ million

The biggest driver of this net short position has been bilateral currency swaps obtained by CBSL, with the 2015-2016 and 2021-2024 having the largest such bilateral swaps. During 2015-2016 this was the large swaps from the Reserve Bank of India (RBI), then in Dec 2021 the decision to draw the People’s Bank of China swap into reserves, and the decision in Oct 2023 to restructure the ACU debt into a $2.6bn swap with RBI. However, beyond the bilateral swaps the net short position also includes FX swaps between CBSL and the domestic banks, as has been noted by IMF reports. The short position swaps allow CBSL to essentially borrow FX from local banks to boost FX reserves, without purchasing the FX in return for a permanent injection of rupees.

During the 2016-2019 IMF program, most of these swaps were wound down, reducing the net short position to less than $500mn in late-2019. Part of the external FX borrowings during this period went into this action which improved the quality of the FX reserves position. But that improvement was fully reversed in the next few years.

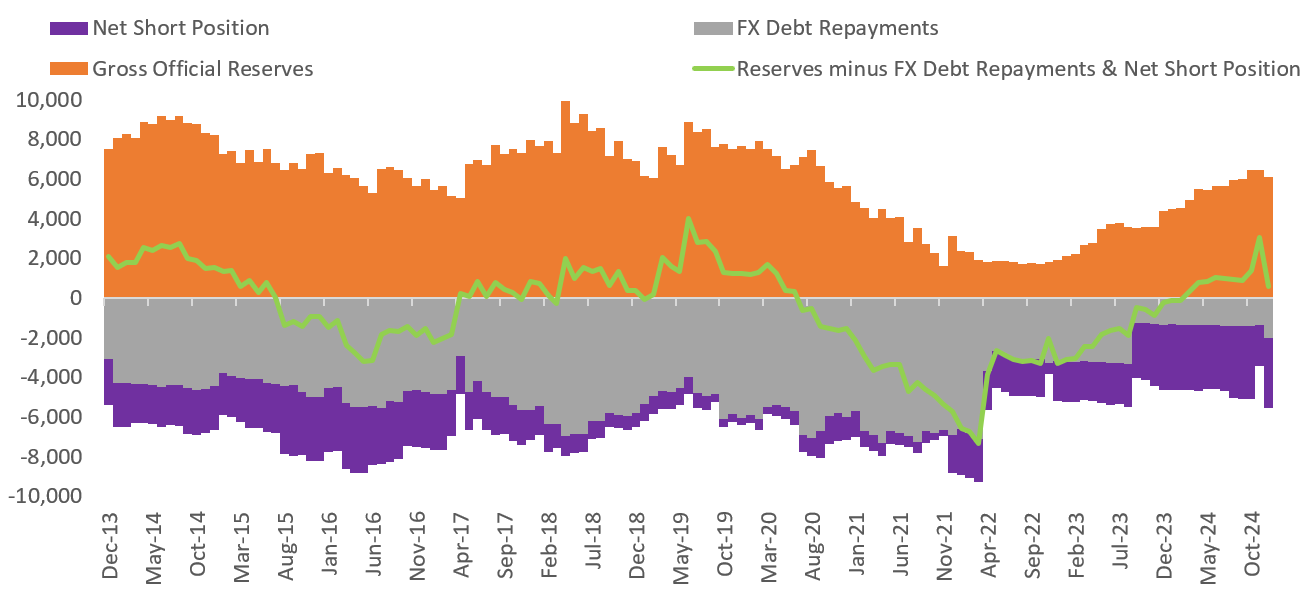

Only for short periods of time have CBSL FX reserves have been substantially higher than FX debt repayments and net short position since 2014, highlighting the challenges of reserves buildup.

Figure: CBSL FX Reserves vs. Pre-determined FX net drains (debt repayments & net short position), $ million

Of course, not all the net short position is repaid in full each month. Bilateral currency swaps have particular maturity periods and repayment schedules (though those might be adjusted under bilateral agreements between central banks). For instance, the $400mn RBI swaps are usually available for about 3 to 9 months, though the one given in Jan 2022 was only being repaid from Nov 2023 onwards until Sept 2026 (alongside the $2.2bn in ACU debt). In comparison, most of the rest of the swap (largely from domestic banks) are assumed to be capable of being rolled over unless settled by CBSL.

Exceptional case since crisis

Since late 2023, both SLDB and ACU related payments have not been covered since SLDBs were fully restructured away and ACU dues were restructured into an RBI swap. Therefore, since late-2023 the pre-determined outflow data essentially covers ongoing repayments to multilateral creditors - mostly by the central govt but also on the past IMF loans taken by CBSL.

The latest data available from pre-determined FX debt outflows for 2025

The Nov 2024 FX debt outflows data (that is excluding net short position), showed $1.36bn in repayments during Dec 2024 to Nov 2025, which indicates about $1.2bn in repayments during Jan-Nov 2025. The Dec 2024 data showed a significantly higher value of $2bn for Jan to Dec 2025. This ~$800mn increase can be attributed to the impact of the ISB restructuring finalized in Dec 2024. After the ~$500mn in repayments in Dec 2024, there are about $720mn in repayments due in 2025 on the ISBs alone.

An interesting thing I notice in the data is that the bi-annual ISB repayments now seem to be due in June and December, rather than in March and September as earlier expected, given the increase in repayments post ISB restructuring has happened in the Apr-Dec period in the data than in March. This makes sense given the new ISBs were issued in late-Dec and six months from that is June.

Technically, the $2bn in FX debt repayments should include interest payments on the $1.1bn in USD bonds issued to domestic banks that took the local option in the ISB restructuring. But the coupon rate in 2025 for these bonds is only 1%, which means only $11 million in repayments on these bonds. In addition, it’s likely that there is about $30-50 million in repayments to the domestic banks on their Past Due Interest (PDI) bonds. Therefore, close to 10% of repayments on the ISBs in 2025 might be going to the domestic banks, rather than flowing directly to foreign ISB holders.

However, the $2bn in FX debt repayments shown in the data is not all the FX repayments that the Treasury and CBSL have to handle in 2025. A big known factor outside of this $2bn is the $900 million in annual repayments on the $2.6bn RBI swap being repaid as $75 million monthly repayments from Nov 2023 to Sept 2026. This is part of the net short position outflows, since its related to a swap.

Figure: Pre-determined FX debt repayments over next 12 months in Nov & Dec 2024 pre-determined data, $ million

Using MoF documents & RTIs to verify debt repayments

External debt repayment forecasts of the government obtained from the External Resources Department (ERD) in June 2024 (via RTI) showed about $1.1bn in debt repayments to multilaterals in 2025. Beyond this there is likely $250-300 million in repayments to be made by CBSL to the IMF on the loan taken during the 2016-2019 IMF program, which is not covered in the ERD data.

After completing the external debt restructuring in Dec 2024, Secretary to Treasury Mahinda Siriwardana stated in a speech in January 2025 that the repayments on restructured debt in 2025 is likely to be about $1 billion. This $1 billion would cover the restructured ISBs (about $720mn), other commercial and bilateral debt (remaining ~$300mn). The chart from the Secretary's speech shows the repayments due on the current stock of external debt, so it would rise with future external borrowings.

So, for 2025 the combined data from these sources gives a repayment number of just above $3 billion. This includes ~$1bn on the bilateral and commercial debt, ~$1.1bn on the multilateral debt repaid by the Treasury, ~$250-300mn in IMF loan repaid by CBSL, and $900mn in RBI swap repayments by CBSL. That gives a $3.2-3.3 billion in external repayments for 2025.

Figure: Rough estimate of external repayments in 2025, $ billion

Going into 2026-2027, the repayments on the RBI swap would reduce to $650mn in 2026 and zero in 2027, while multilateral repayments by the Treasury are likely to rise to $1.3bn or so by 2027. So, the external repayments are likely to be lower in 2026-2027 then in 2025, before of course rising significantly from 2028 onwards as ISB repayments rise.

Beyond all this what we don’t know of course is how much external debt repayments the SOEs have to make. Some of their external debt to foreign creditors, including Chinese ones, were restructured. The other is we don’t know the exact debt repayment obligations of the private sector and banks. However, these combined are unlikely to be more than 20-30% of the government and CBSL’s external FX repayments.

The analysis and opinions herein are my own, based on the overall macro work I do. The data of course is based on the latest available public and RTI data I have at hand. Others may have more up to date and more in detail data than this. I hope that the CBSL or MoF releases better future FX repayments data, without the market having to depend on guesstimates like this. I hope this article also serves as a guide to anyone trying to better use the CBSL’s pre-determined FX net drains data.