Open Market Operations, FX purchases & Liquidity in Sri Lanka

A brief explanation & history of CBSL's market liquidity interventions

Over the last decade, Sri Lanka has seen increasing public discourse about the central bank’s role in ‘money printing’ and ‘rupee liquidity injections.’ These topics gained substantial prominence with Sri Lanka’s economic crisis in 2021-2023. The ability of central banks to create domestic currency out of thin air, through a few digital key strokes, has always been both a fascinating and scary phenomenon. This ‘accounting magic’ is most useful when financial markets are in dire need of liquidity. But when overdone, especially in the form of monetary financing of the fiscal deficit, this ‘magic’ can have severely negative impacts as Sri Lanka’s crisis showed.

The main avenue of what is colloquially termed ‘money printing’ that was identified for reform post-crisis, under the 2023 CBSL Act, was to put heavy restrictions on the CBSL’s ability to purchase government securities at primary issuance (directly from Treasury), except in emergency situations for short 6 month periods. Discussion on this monetary financing of the fiscal deficit will be left for another time.

CBSL of course retains its ability to purchase government securities in the secondary market as part of its open market operations (OMOs). OMOs are the primary way in which central banks intervene to manage financial market liquidity conditions, which in turn affects interest rates and lending by financial institutions (FIs). CBSL FX interventions can also have impacts on liquidity, since those also utilize the central bank’s domestic currency creation powers.

CBSL’s current monetary policy involves the Overnight Policy Rate (OPR), which takes the immediate target as the Average Weighted Call Money Rate (AWCMR) - the rate at which interbank uncollateralized lending happens. CBSL can use OMOs to inject liquidity if AWCMR is significantly above the OPR or absorb liquidity if AWCMR is significantly below the OPR, attempting to get the rate in line. But slight deviations tend to be ignored, allowing the market to adjust as needed.

The purpose of this article is to provide an overview of what the OMO and FX intervention instruments CBSL has at hand, their actual usage based on data available, and what their impact on liquidity can be. It does not attempt to analyze whether CBSL actions had anything to do with recent currency volatility.

What are the main OMO instruments?

OMOs are largely done through transactions that involve the use of government securities (except SDF). These involve qualified financial institutions - mostly licensed banks and primary dealers. The OMO channels used in Sri Lanka are explained briefly and their use visualized using CBSL documents and market operations data in the subsequent sections.

Standing Overnight Facilities:

Not exactly OMOs on a tight definition, but these standing facilities when used as overnight facilities affect LKR liquidity conditions.

Standing Lending Facility (SLF) - Liquidity Injection - Qualified FIs can borrow LKR overnight from CBSL, with g.secs used as collateral, to meet any shortfalls in their balance sheets at the SLF interest rate. It operates similar to a reverse repo described below.

Standing Deposit Facility (SLF) - Liquidity Absorption - Qualified FIs can deposit excess LKR overnight at CBSL at the SDF interest rate.

SLF and SDF are freely available to utilize by qualified FIs, with no explicit limit to the amounts utilized. SDF tends to have some utilization on a daily basis, while SLF can have days of non-utilization. It is not an active decision by CBSL to offer these facilities each day. Utilization depends on the FIs needs.

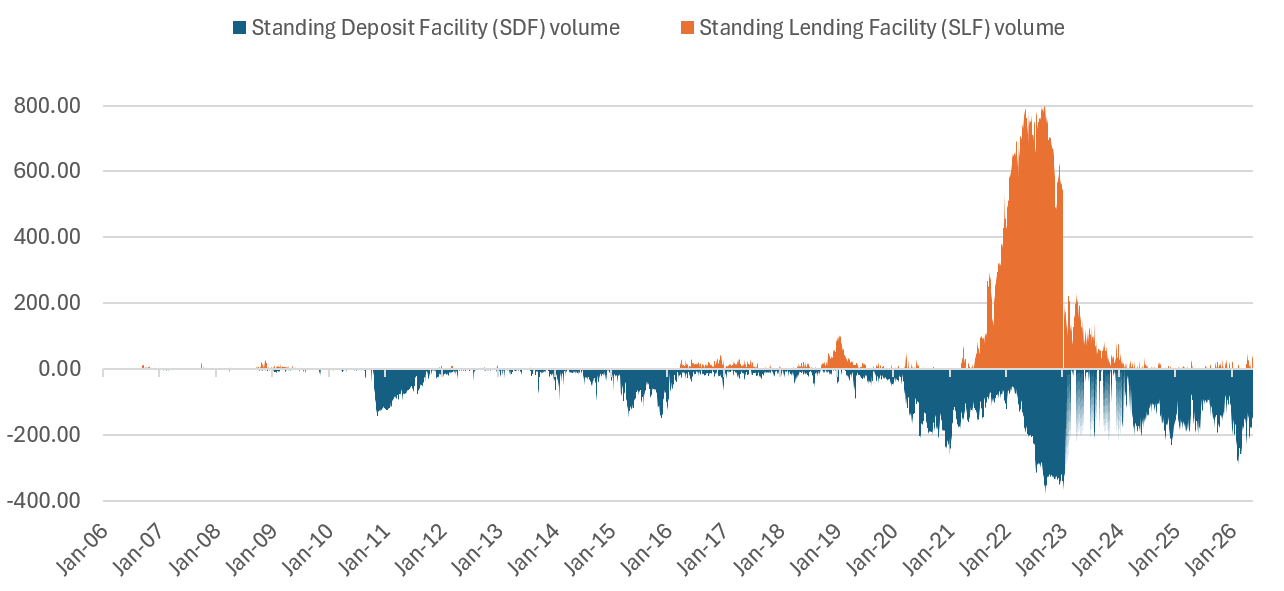

As the chart shows, there were sustained periods in 2011-2012, 2015-2016, 2020-2022, and 2023-2026 that saw large SDF volumes. SDF volumes being high does not necessarily mean positive overall liquidity conditions. It can also mean that some FIs choose to park their money at the CBSL, one of the safest possible options, instead of lending or investing in the real economy. This was especially the case since 2020 for foreign banks in Sri Lanka. Many of the local banks ended up borrowing substantial amounts from CBSL through SLF during 2021-2023, reaching almost LKR 800 billion, even as the foreign banks maintained large balance under SDF.

SLF and SDF volumes, LKR billion

(SDF absorption shown as negative & SLF injection shown as positive)

Unlike the standing facilities, the Repo and Outright OMOs are active OMO instruments where the CBSL decides on the timing and magnitude of OMO intervention it wants to conduct in each instance.

Repo Facilities:

Repos - Liquidity Absorption - In a repo auction, CBSL temporarily sells government securities to FIs with an agreement to buy them back at a pre-agreed future date, which removes (absorbs) excess rupees from the financial system for that time period. Overnight repos absorb liquidity for one day, while term repos can apply for a few days, few weeks or even a couple months.

Reverse Repos - Liquidity Injection - In an overnight reverse repo auction, CBSL temporarily buys government securities to FIs with an agreement to sell them back at a pre-agreed future date, which adds (injects) excess rupees to the financial system for that time period.

The CBSL’s domestic operations department must decide when to hold such auctions and the maximum size of the auctions based on the liquidity conditions. But the final amount accepted would also depend on the demand and bids from the FIs.

Operationally, CBSL considers overnight to one week repos as short-term repo auctions and those above one week as long-term repo auctions. Functionally, repos are settled by 08.30am and reverse repos are settled by 11am according to the Consolidated Operating Instructions on Market Operations. Since they are finalized by 1.15pm on the day of the auction, an overnight repo is pretty much overnight, lasting from the afternoon of the auction to the next working day morning settlement.

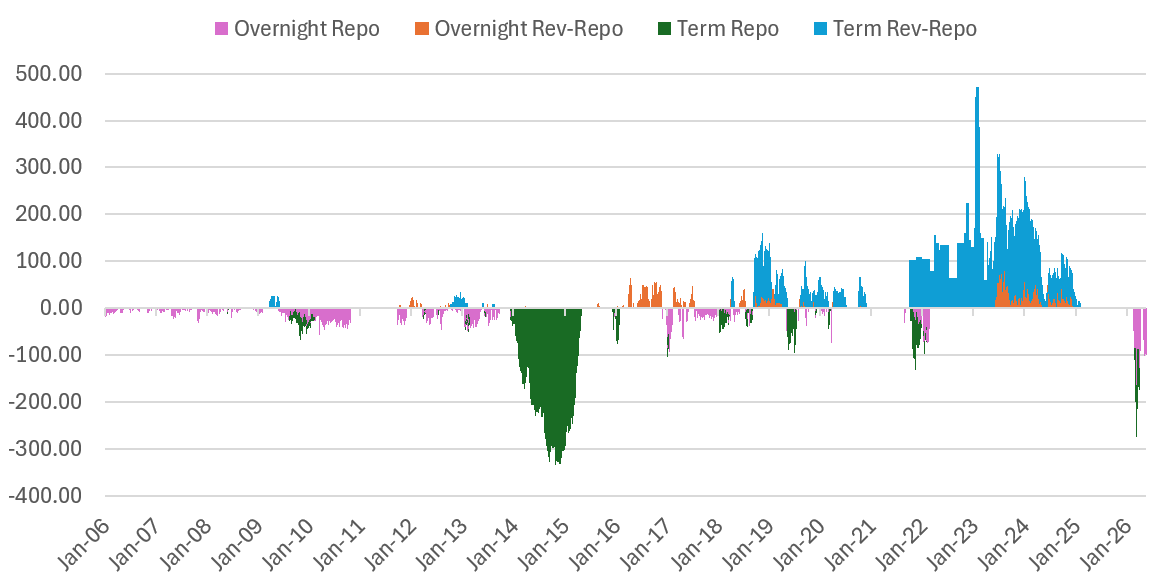

The repo facilities have been utilized intensely only in some period. In 2014-2015, term repos were utilized heavily to absorb excess liquidity, while the use of overnight and term repos since Feb 2026 has also been substantial. On the other hand, term reverse repos were utilized significantly in 2018-2019 and 2022-2024 to inject liquidity.

CBSL Repo & Reverse Repo Volumes, LKR billion

(Repo absorption shown as negative & Reverse Repo injection shown as positive)

Outright Transactions:

SLF, SDF and repo facilities involve a temporary transaction between CBSL and FIs. They are unwound within a pre-determined time period. However, if the central bank wishes to, it can outright purchase government securities from the secondary market, causing a long-term injection or removal of financial market liquidity. Sometimes such transactions can be done to adjust liquidity and yields of particular tenures of government securities as well.

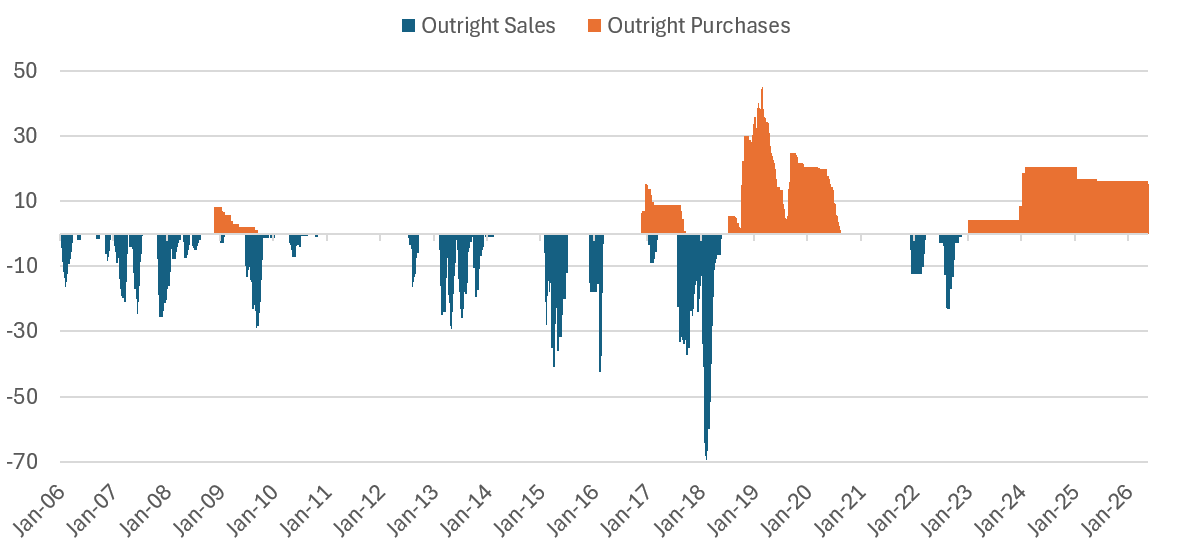

As visible below, in periods like 2013, 2015-2016, and 2018 saw outright sale of G.secs that were held by CBSL to absorb liquidity. In periods like 2019-2020 and 2023-2026, outright purchases were deployed to inject liquidity. The maturity period of the purchases done in 2023-2024 were longer, resulting in their impact running for a prolonged period. But overall, the liquidity impact from outright transactions has been much smaller than the other OMO instruments.

CBSL Outright Transactions Volumes, LKR billion

(Sales are absorptions shown as negative & Purchases are injection shown as positive)

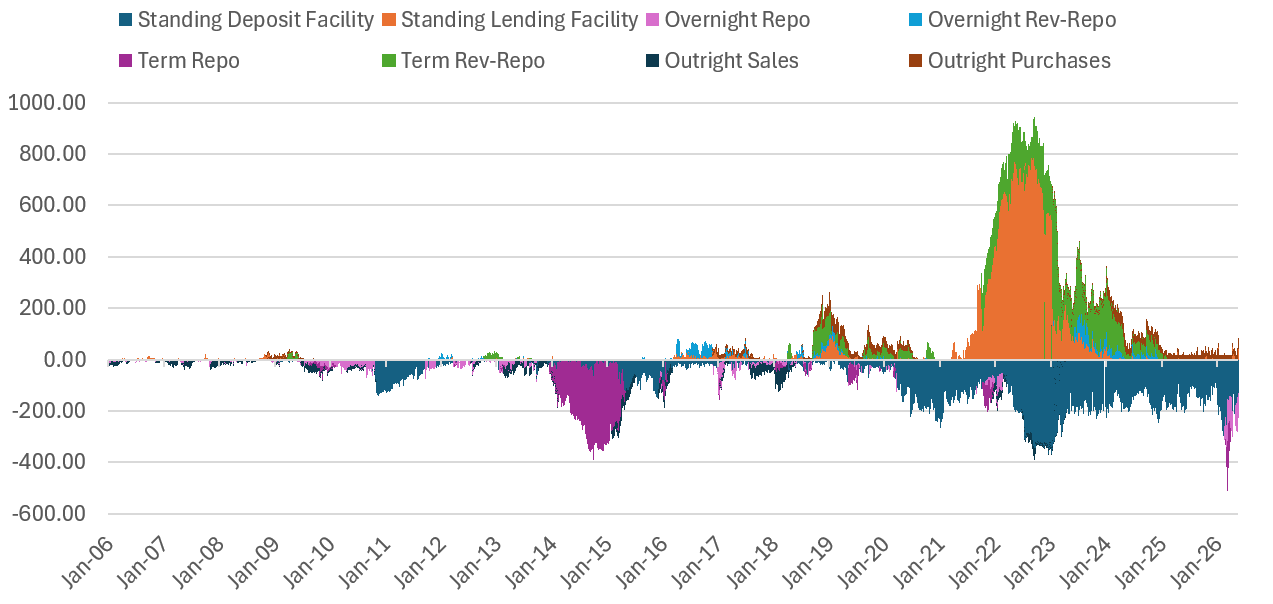

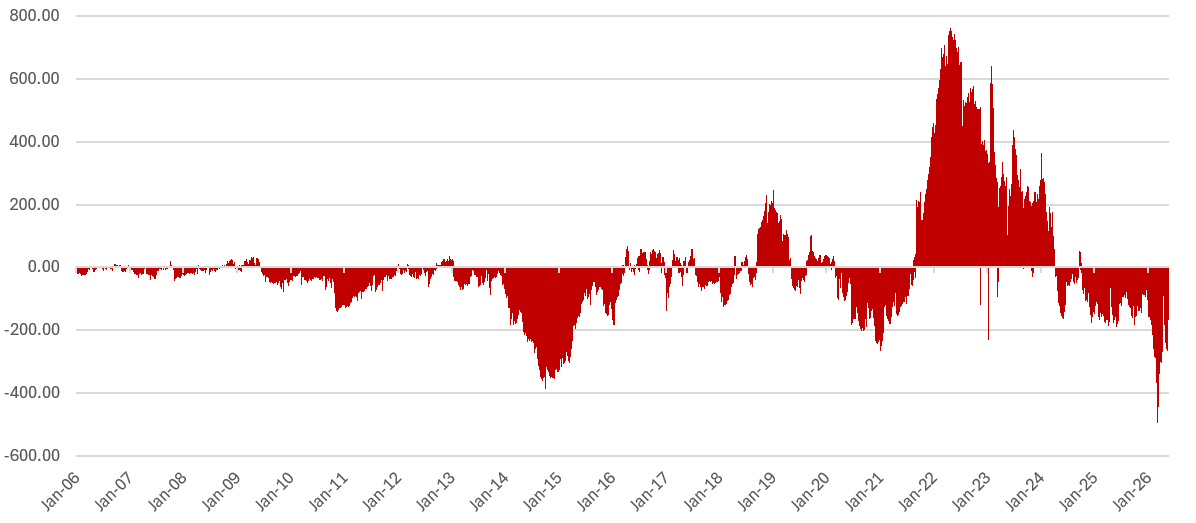

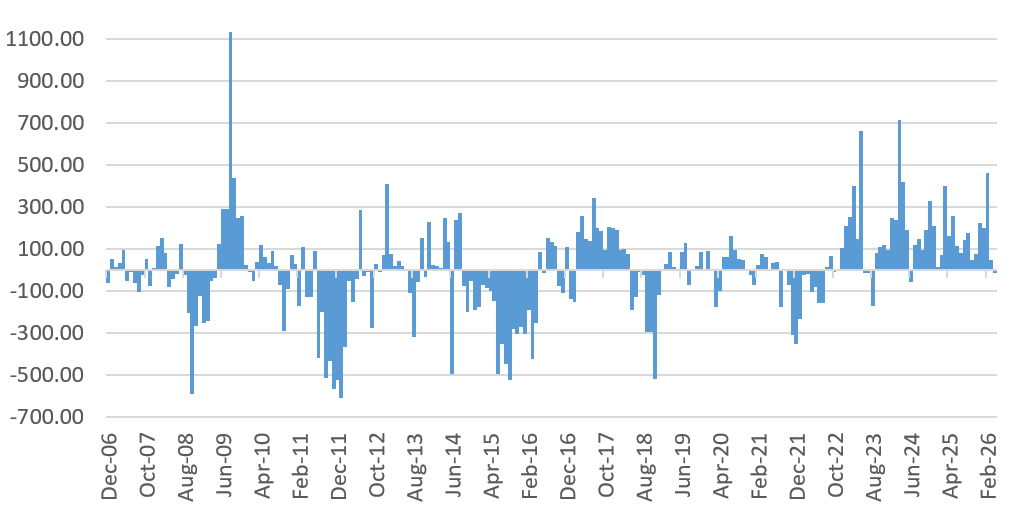

The combined liquidity impact of these main standing and OMO instruments can be quite substantial in certain periods, and almost absent in others.

CBSL main OMO instrument outstanding volumes, LKR billion

(Absorptions shown as negative & Injections shown as positive)

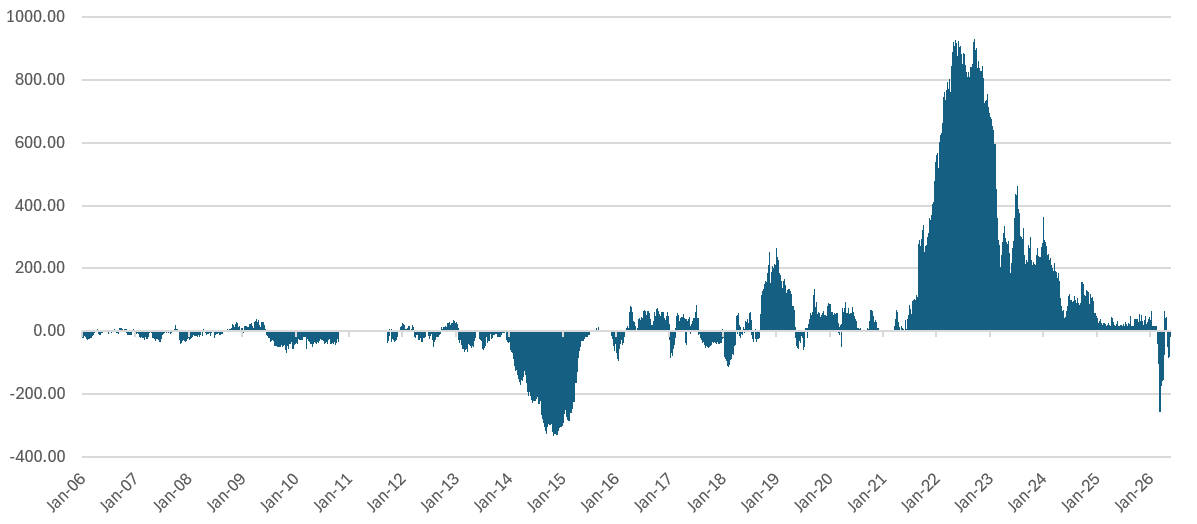

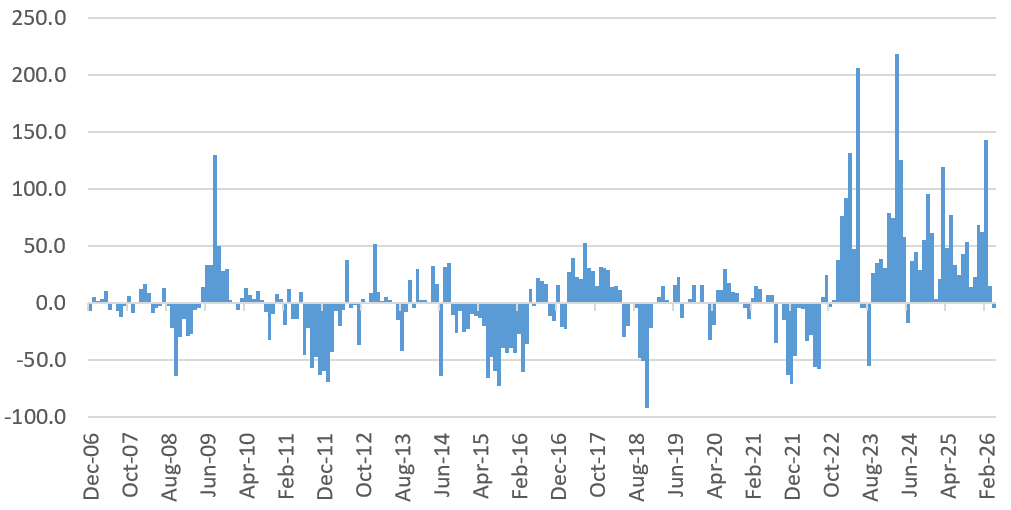

When the injections and absorptions are netted, one can get a clear picture of the net impact on LKR liquidity from OMOs.

Net Liquidity Impact from OMO outstanding volumes, LKR billion

(Net Absorptions shown as negative & Net Injections shown as positive)

Given the SDF usage is based on decisions by FIs to deposit their excess LKR with CBSL, and does not reflect CBSL’s power to create LKR out of thin air, I prefer to look at the OMO net impact excluding SDF. It shows that the net liquidity impact from OMOs has been substantial, in either direction, only in some periods like 2014-2015 (absorption), 2018-2019 (injection), 2021-2024 (injection), and in early-2026 (absorption).

Net Liquidity Impact OMO outstanding volumes excl SDF, LKR billion

(Net Absorptions shown as negative & Net Injections shown as positive)

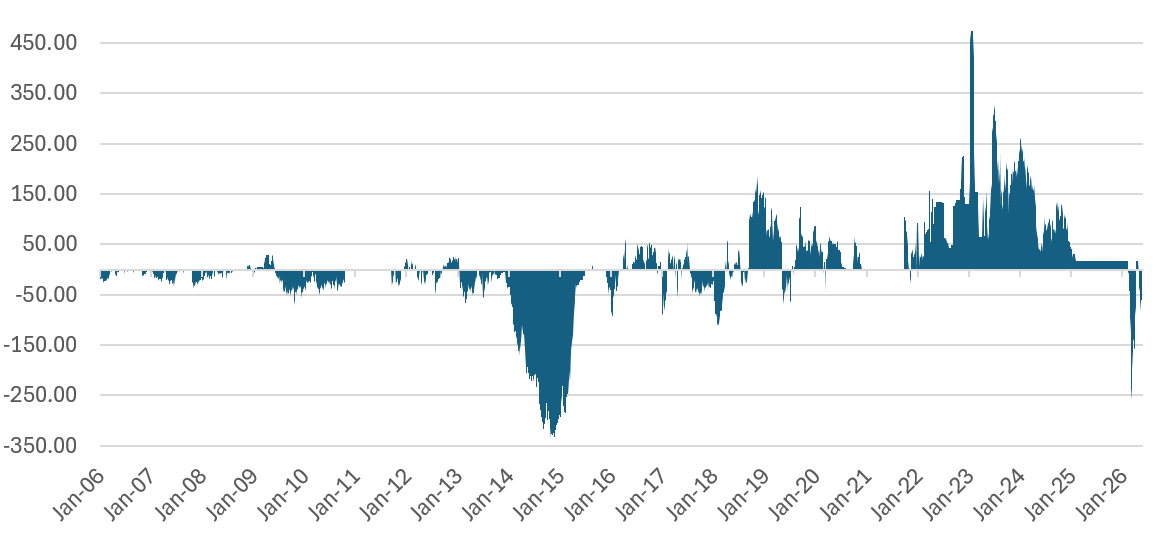

If one only looks at the active OMOs, that is excluding both SLF and SDF, then the net impact is substantially lower. With highest injections being during 2018-2019, 2022-2024, and largest absorptions being in 2014-2015 and early 2026.

Net Impact of Active OMO outstanding volumes (excl SLF & SDF), LKR billion

(Net Absorptions shown as negative & Net Injections shown as positive)

Any other CBSL LKR liquidity instruments?

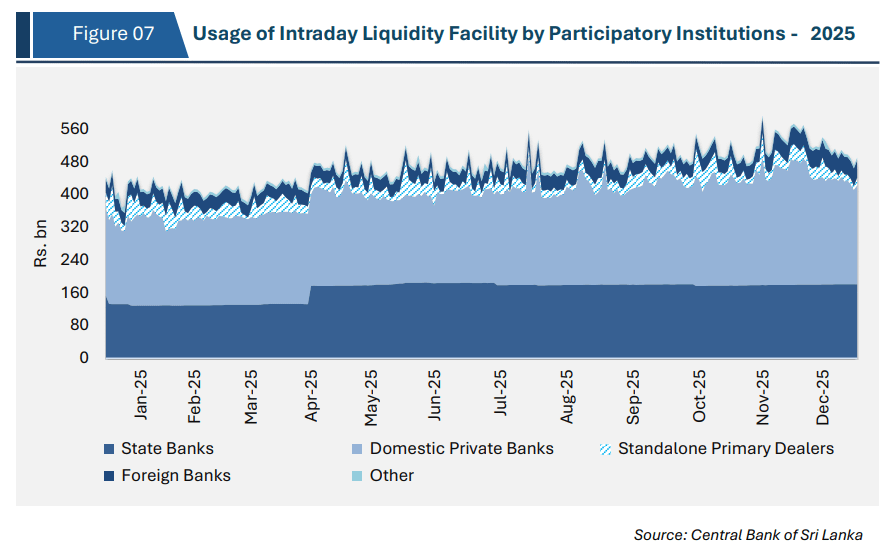

Beyond these major instruments for which we have daily data, CBSL also has an Intra-day Liquidity Facility (ILF) available for eligible FIs, mostly banks and primary dealers, to ensure the smooth operation of the Real Time Gross Settlement (RTGS) system that handles bulk payments between FIs. The daily average volume of the ILF utilization was as high as LKR 467.7 billion in 2025 according to the December 2025 Monetary Operations Report of CBSL. But ILF liquidity is settled within the day, leaving no net impact on the liquidity situation at the end of the day. Any remaining liquidity shortfalls at the end of the day must be met by other means, including the main standing and OMO facilities discussed above.

An FI doesn’t have to resort to borrowing from CBSL. It can also resort to the call money market and the repo market to borrow from other FIs with excess LKR. That’s a topic for another day.

Beyond these routine instruments, in an exceptional situation the CBSL can extend Emergency Loans and Advances (ELA) to a bank in distress to ensure financial system stability.

LKR liquidity impact from CBSL FX interventions

Even if CBSL is not doing significant OMOs, it can also affect LKR liquidity in financial markets through its FX activity.

Purchase and Sale of FX from FIs

As part of its reserve and exchange rate management, CBSL routinely buys and sells foreign currency from financial institutions, primarily banks. When it purchases FX, CBSL reduces the FX in the banking system and injects LKR liquidity into the banking system. When it sells FX, CBSL injects FX liquidity and absorbs LKR liquidity from the banking system. Unfortunately, the daily FX intervention data is not available, only the monthly aggregate sales and purchases.

Depending on the priority of CBSL, the direction and magnitude of these FX interventions can vary. 2009-2010, 2016-2017, 2023-2026 have been periods with sustained and substantial net FX purchases, while 2008-2009, 2011, 2015-2016, 2018, 2021-2022 have been periods with sustained and substantial net FX sales.

Monthly Net FX Purchases by CBSL, USD million

(Net Sales are negative & Net Purchases are positive)

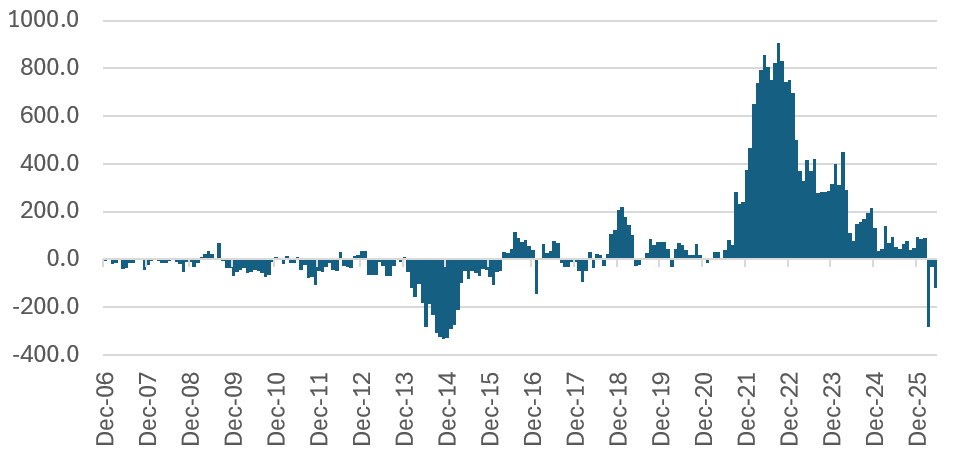

Due to LKR depreciation, the monthly LKR impact is larger now compared to late-2009, even though the net purchases in late-2009 was higher. While there was about an LKR 300 billion LKR liquidity absorption due to net FX sales in 2021-2022, the net FX purchases across 2023 to Apr 2026 has injected about LKR 2.2 trillion in LKR liquidity into the financial system.

Monthly Net FX Purchase LKR impact, LKR billion

(Net Sales are negative & Net Purchases are positive)

Domestic FX Swaps

Just like with government securities based repos for OMOs, CBSL can do short-term transactions for FX through FX swaps with domestic banks. It is an instrument that can help manage both FX and LKR liquidity conditions. In CBSL guidelines, this is considered an active OMO instrument.

CBSL can provide FX to banks for a short period (while taking LKR from the banks in return) via sell-buy swaps, reducing gross reserves. CBSL can borrow FX from banks (in return for LKR provided to the banks) for a short period through buy-sell swaps, raising gross reserves.

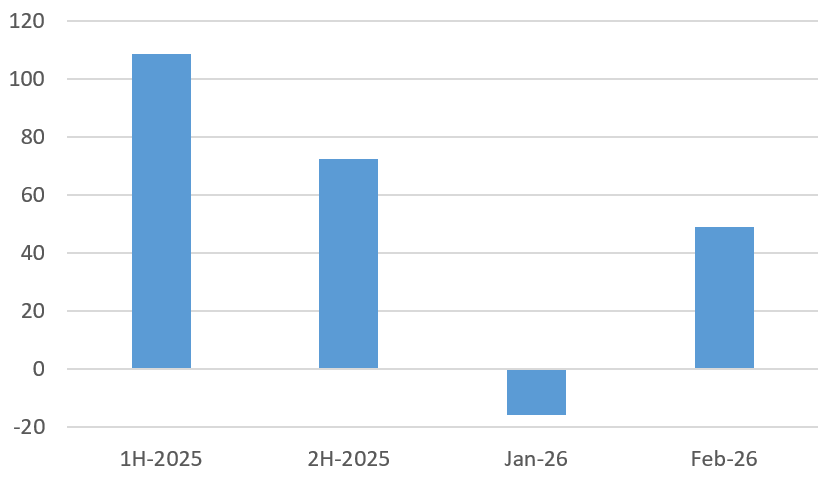

Unfortunately, we don’t have regular data on the domestic swaps outstanding until recently, with bi-annual data in the monetary operations data since 2024 and monthly data in monthly data since Dec 2025. For the period 2025 to Feb 2026, the outstanding buy-sell FX swaps, where CBSL borrows FX, has increased from USD 1.3 billion to USD 2 billion. The LKR liquidity injection impact from this increase has been about LKR 215 billion.

Monthly Net Domestic FX Swap LKR liquidity impact, LKR billion

Treasury FX transactions with CBSL

The only way the Treasury (Ministry of Finance) is able to obtain FX directly is through foreign debt issuance, foreign grants received, and any state assets sales to foreigners (like the Hambantota Port lease back in 2017).

If the Treasury wants LKR instead of the FX it holds, it can sell the FX to CBSL in return for LKR. In effect the CBSL provides freshly created rupees to the Treasury. If the Treasury wants FX, it can buy from CBSL with LKR it holds. Treasury can source LKR mostly from revenue and LKR debt issuance (or CBSL could directly lend the Treasury LKR as well (through provisional advances for instance, but lets leave that scenario out for now).

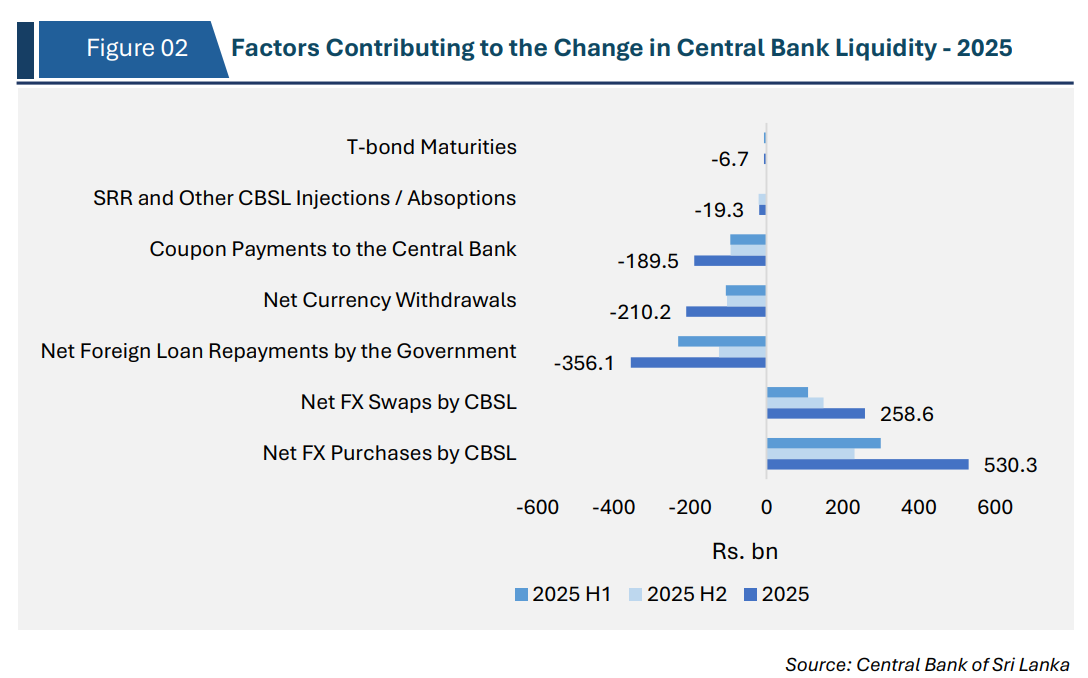

In effect, through this transaction also CBSL can inject or absorb LKR liquidity from the economy, through the Treasury. In 2025 for instance, CBSL notes that Treasury net purchased about LKR 356 billion (~USD 1.1 billion) worth of FX from CBSL, which was a liquidity absorption by CBSL. But in 2024, Treasury net sold about LKR 97 billion (~USD 300mn) worth of FX to CBSL, which was a liquidity injection by CBSL.

Can we estimate a net impact over time?

What we have discussed above does not cover all the channels through which CBSL can affect LKR liquidity conditions. But they are the most relevant when we consider OMOs and FX intervention channels we wanted to focus on.

What’s covered is also what we have regular data for. In trying to combine the OMOs and FX interventions to get a picture of the net impact, we can take the average monthly OMOs outstanding and the monthly net FX sales and purchases data. While that excludes the domestic FX swaps and Treasury FX transactions with CBSL, it still covers a substantial portion of CBSL LKR liquidity actions as shown in the chart above for 2025.

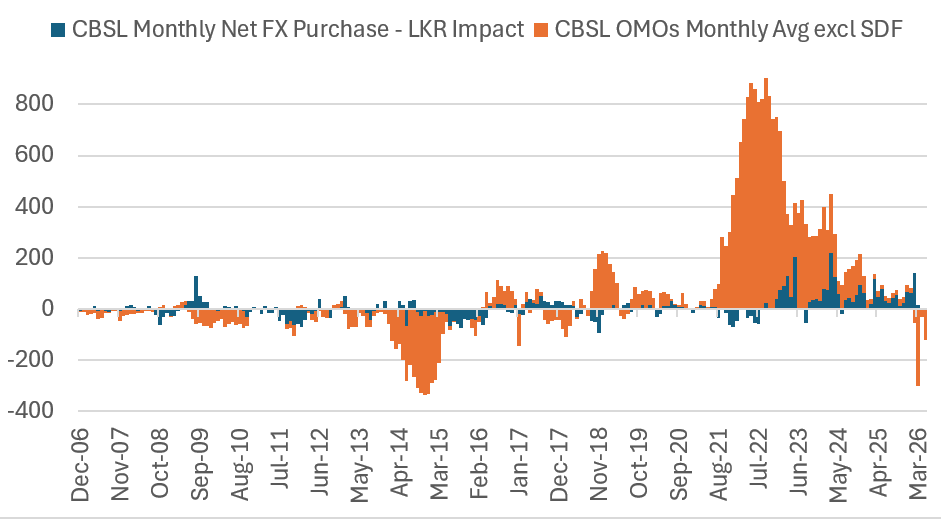

What is clear is that since 2023, Net FX purchases have emerged as a major LKR liquidity injection, surpassing impact of OMOs. Since 2025, FX purchases are almost the only source of CBSL LKR liquidity injections. But in early-2026, CBSL engaged in active OMOs to absorb excess liquidity in the financial market, the largest such operation in LKR terms since 2014-2015.

The role of FX intervention would be higher when considering the increase in domestic FX swaps, for which we lack publicly available monthly data going into the past, preventing its inclusion in the charts below.

CBSL OMO & Net FX Purchase impact on LKR liquidity, LKR billion

(Net Absorptions shown as negative & Net Injections shown as positive)

CBSL OMO & Net FX Purchase aggregate impact on LKR liquidity, LKR billion

(Net Absorptions shown as negative & Net Injections shown as positive)

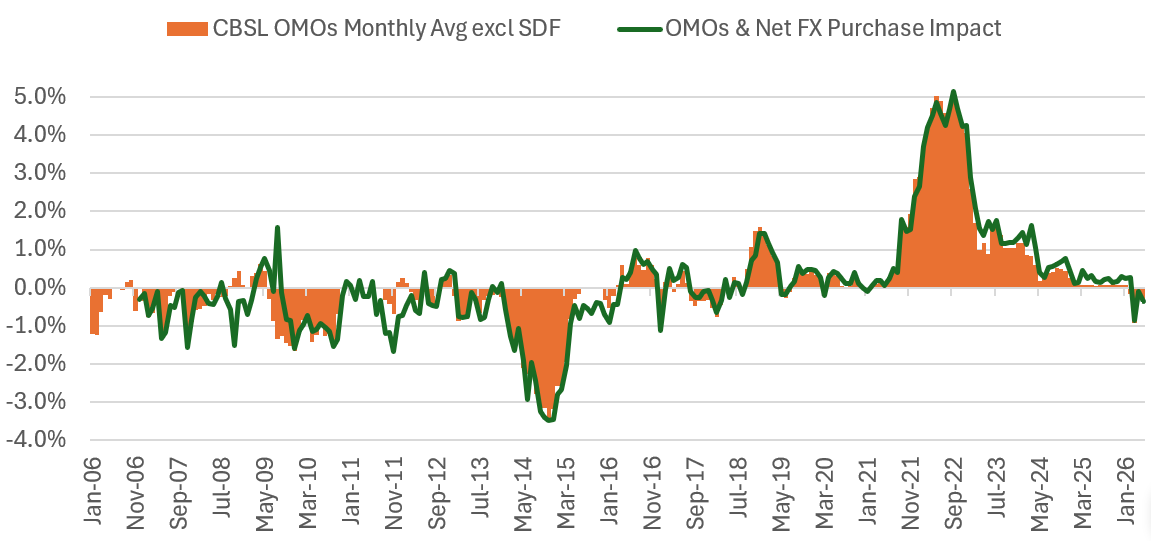

To provide a comparative analysis of the extent of these rupee impacts, the monthly OMO and Net FX purchase impact on LKR liquidity can be looked at as a share of the previous year’s nominal GDP. It shows that despite the rupee values being smaller, there were multiple periods where the liquidity impact was around or exceeding 1% of GDP on multiple occasions in either direction. 2014-2015 and 2021-2022 are clearly the outliers in terms of the extent of liquidity absorption and injection.

CBSL OMO & Net FX Purchase Monthly impact on LKR liquidity,

% of previous year GDP

(Net Absorptions shown as negative & Net Injections shown as positive)

Disclaimer: This article is based on my personal analysis and views, taking into account official documents and data that are publicly available, and is completely independent of any institutions that I am affiliated with.

My interest in OMOs and FX intervention has been particularly driven by the continuous coverage of these by EconomyNext and its long-time columnist Bellwether.