Sri Lanka's Post-Default Macro - Sovereign Default & External Surpluses

A look at the numbers behind the strengthening of the LKR

From the start of 2023 to mid-2024 Sri Lanka’s interest rates have reduced around 2000 basis points (12 month T-bill rates above 10%) and the LKR has appreciated about 16% against the USD to around 300/$. At the height of the post crisis messiness, Sri Lanka saw an exchange around 360/$, 12-month T-bill rates around 30% in early 2023 and policy rates of 16.5%. The reduction from these peaks has been despite the country continuing to be in sovereign default, and working towards restructuring deals that have finally almost been reached in Jun/Jul 2024. The IMF in its 2nd review of the program has commended this macro stabilization, that has happened earlier than expected, even though risks continue to exist.

The other three developing countries that have gone through external debt restructurings alongside Sri Lanka - Zambia, Suriname and Ghana - have seen improvements but not to the same extent. On the exchange rate, Zambia and Ghana have both seen significant depreciation since 2023, while Suriname has seen some appreciation since mid-2023 and Zambia since start of 2024 helped by progress on debt restructuring. Yet, on interest rates Suriname continued to suffer 45% interbank rates in April, while Ghana has 29% policy rates and Zambia has continued rate hikes to 13.5%.

Figure: Depreciation against USD, % change at end-June 2024

What’s Sri Lanka been doing?

Exchange rate & Interest rates are simply outcomes of the broader macro stabilization achieved. Of course, that stabilization has come at the cost of growth, increased poverty, and lowered/stagnating standards of living for most of the population. Real GDP growth only began to move towards positive territory from 2H-2023 onwards. Yet, real GDP levels remain well below pre-crisis and would take till 2027 to get back to above 2018 peak if growth averages 3% from 2024 onwards.

Figure: Real GDP growth picking up since 2H-2023

Figure: Real GDP level remains below pre-crisis

Understanding what is behind the LKR appreciation

The obvious and straightforward answer is that Sri Lanka has been recording quarterly current account surpluses since 3Q-2022 and will likely continue to do so in 2024 as well. No time in the past has Sri Lanka managed to record such consecutive current account surpluses. But even those surpluses are simply an outcome of other factors at play - the sovereign default and the tight fiscal and monetary policies since April 2022.

Impact of the sovereign default

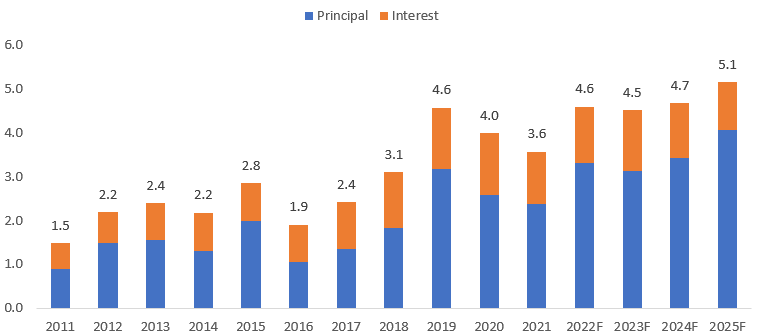

Pre-default, the central government external debt repayment schedule had Sri Lanka committed to a daunting task with $4.5-5bn in annual repayments. And that’s before accounting for FX debt obtained domestically by the government and foreign liabilities of CBSL. Getting through 2022 without default would have involved handling over $7bn in FX repayments by the government and CBSL. The 12th April 2022 decision to suspend most external debt repayments of the government led to the reduction of those repayments.

Figure: Central Government External Debt Repayments actual forecast at end-2021 (pre-default), $ billion

The IMF program’s debt targets involved reducing external debt repayments of the government during 2022-2027 and that’s part of what has been achieved with the debt restructuring deals. Even with repayments likely to restart from late-2024, the repayments are going to be much less than pre-crisis forecasts (at least until 2028/2029).

Figure: Central Government External Debt Repayments actual up to 2023 & estimates for 2024-2025 (based on recent debt agreements)

There has been total current account surplus of $2.5bn since 3Q-2022. But this includes the interest Sri Lanka has not been paying on its external debt since April 2022. This is because the accrued interest arrears is offset by incurring a new external liability on the financial account. As a result, when the accrued interest arrears accounting entry is excluded, the current account surplus is $4.5bn for these past seven quarters.

Figure: Quarterly Current Account Surpluses - with & without Accrued Interest Arrears, $ million

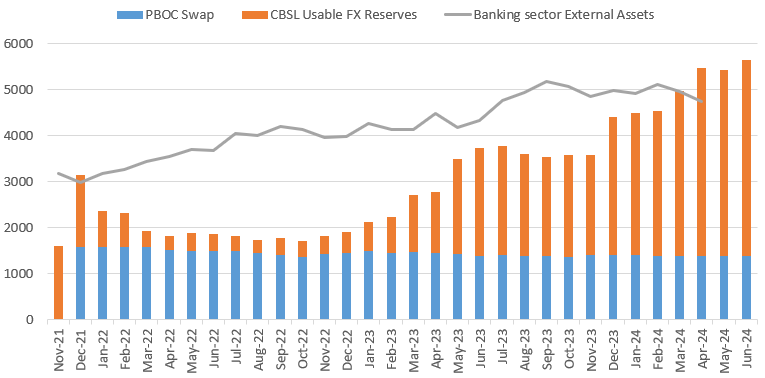

Most of this current account surplus has been purchased into CBSL’s FX reserves or improved the net foreign assets of the banking sector, increasing Sri Lanka’s international reserves position significantly. CBSL’s Usable FX reserves (excl the PBOC swap) increased by around $4bn from Aug 2022 to June 2024, driven by $4bn in net FX purchases from the domestic banks and government retaining a significant portion of the multilateral disbursements in its CBSL accounts. This is even as CBSL likely paid about $1.4bn in external liabilities and govt made over $3bn in external repayments to multilaterals and India during the same period.

Figure: Foreign debt disbursements to Public sector, $ million

Loan disbursements by multilateral lenders amounted to around $3.5bn since April 2022, helping to finance the external debt repayments (to the multilaterals and India mostly) handled by the government and CBSL since then. The crisis has significantly increased dependence on multilateral financing (IMF, ADB, WB, AIIB, and others) which have been the largest source of foreign financing - especially outside of India’s 2022 emergency financing. As above chart shows (in yellow), foreigners did return to invest in rupee govt securities in 2023 (mostly in 1H 2023), but since then have been gradual net outflows.

Figure: CBSL & Banking sector international reserves, $ million

Low imports as driver of current account surplus

The recovery in tourism and remittance earnings back towards pre-crisis levels is the good news that has been helping towards a current account surplus. As I have noted earlier, growth in port services is also helping. The bad news that’s been contributing to it is monthly non-fuel imports remaining at 10-yr lows (excl 2020 pandemic impact), despite some recovery since the height of the crisis.

Figure: Non-Fuel imports at 10-yr lows

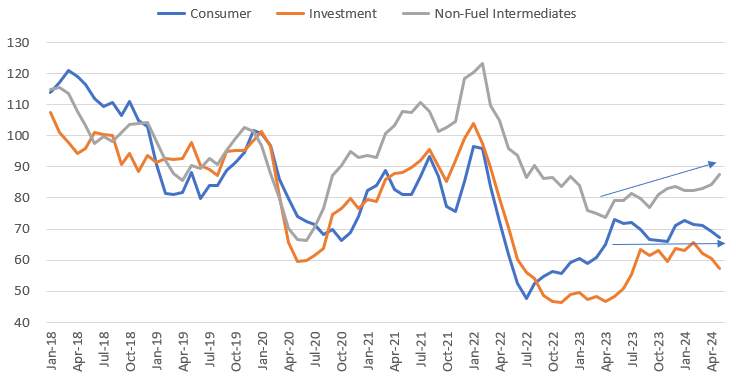

This is seen across most major import categories, each reflecting the suppressed demand conditions across varied economic activities/sectors. The recovery since the post-default low saw consumer and investment goods recovering to current monthly import levels by 2H 2023. But non-fuel intermediate goods have continued to grow since mid-2023.

Figure: Non-Fuel imports by category, 100=Avg monthly imports (in USD) in 2017

This containment in imports is driven by the massive domestic adjustment since the start of the debt crisis period in mid-2021. Loss in real incomes due to high inflation, reduction in disposable income due to rapid rise in income taxes, and credit contraction have severely depleted domestic purchasing capacity relative to pre-crisis. Combined with the lower govt debt repayments, these lower domestic demand means that there is less demand for the USD relative to its improved supply from tourism and remittance recovery. Therefore, it is important to see the external surpluses and LKR appreciation, and reserve accumulation, as partly outcomes of the domestic adjustments. In Part 2 of this, I will be exploring these domestic factors in some detail.

As usual, this is my own analysis and opinions. I focus on providing a look back, in line with my interests in economic history. Frontier Research, where I work, provides clients with more detailed ongoing updates on how the external surplus matters, how it’s linked to domestic adjustment factors. If you are interested in subscribing to Frontier’s reports and outlooks click here.