Sri Lanka’s Public Debt – What is foreign & What is domestic?

An attempt to clarify why the numbers depend on where you look

Ahead of the 30 Nov 2022 release of the China debt paper I co-authored, Rachel Savage of Reuters had a very important clarification on Sri Lanka’s foreign debt numbers. Particularly on why our paper states public external debt is $40.6 billion at end-2021 when the Ministry of Finance says foreign currency debt was $46.6 billion at end-2021 – a massive $6 billion difference! And a similarly wide difference persists in the end-June 2022 data as well. This can cause confusion for anyone trying to figure out Sri Lanka’s debt burden. Ideally at the end of this article, you’ll understand how to work around this complexity.

To this end its essential to understand the three main definitions through which the debt can be broken down:

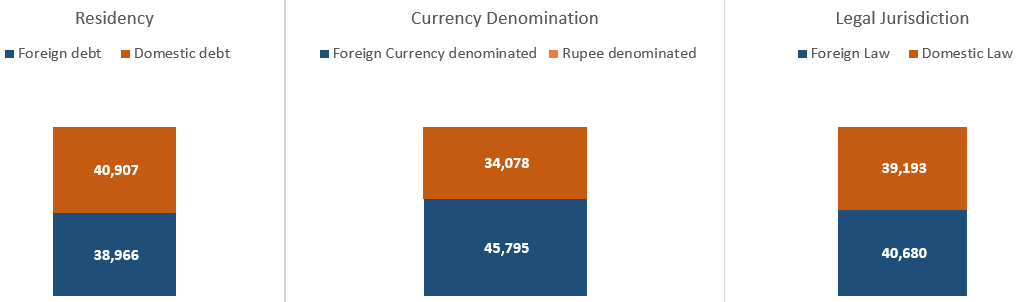

Residency of the creditor/debt holder (non-resident vs. resident or foreign vs. domestic)

Currency denomination of the debt (foreign currency vs. domestic currency)

The legal jurisdiction under which the debt was issued and is governed (foreign law vs. domestic law)

For this purpose, I use the end-June 2022 public debt data available. While the end-September 2022 data is available in a different format to the earlier releases, I have not had the time to process the guaranteed SOE debt data released there.

Figure: Public debt breakdown under the three definitions as at end-June 2022, US$ million

Source: Author compilation based on Ministry of Finance data release and Central Bank of Sri Lanka Monthly Bulletin. Note that the data is subject to revision, so different data releases from the government appear to carry slightly different numbers. Assumptions about arrears calculation and exchange rate can affect the values in dollar terms. But the overall public debt covered in this data is around $80 billion as at end-June 2022.

Residency of the creditor/debt holder

Residency is the primary way in which foreign to domestic debt breakdown is often found in public data releases whether it’s the IMF Article IV documents on Sri Lanka or the Ministry of Finance/Central Bank reports. In this case, neither the currency denomination nor the legal jurisdiction of the debt matters, only whether the current holder of the debt is a resident of Sri Lanka or not.

As a result, foreign currency debt – regardless of being under domestic or foreign law – if held by a resident entity (like a domestic bank) can be considered domestic debt. This has been the case for a portion of Sri Lanka’s International Sovereign Bonds (ISBs), with the domestic banks holding about $1.8 billion of the $12.5 billion outstanding. Since end-2019, CBSL has been reporting this portion of ISBs as domestic debt.

Table 1: Public debt by Residency as at end-June 2022, US$ million

Source: Author compilation based on Ministry of Finance data release and Central Bank of Sri Lanka Monthly Bulletin

Currency denomination of the debt

Currency denomination is important to understand how much of the public debt exposure needs to be repaid in foreign currency versus in rupees. Here there are two major areas where there is clarification:

rupee debt held by foreigners/non-residents. In Sri Lanka this is in the form of rupee Treasury bonds/bills held by foreigners but has become a very small negligible amount since 2019.

foreign currency denominated (dollar denominated) debt held by domestic or resident entities. In Sri Lanka, these can be significant as my conversation with Rachel revealed and, there are a few different types of such debt:

The ISBs held by domestic banks mentioned earlier

Sri Lanka Development Bonds (SLDBs), issued under domestic law, held overwhelmingly by domestic banks and individuals. There is a small non-resident holding of about $25 million.

Dollar denominated loans obtained by the public sector from domestic banks – both by the central government and state-owned enterprises (SOEs) under central government guarantee.

Table 2: Public debt by currency denomination as at end-June 2022, US$ million

Source: Author compilation based on Ministry of Finance data release and Central Bank of Sri Lanka Monthly Bulletin

Legal jurisdiction of the debt

The law under which the debt is issued and governed has implications for the debt restructuring process, since the government of Sri Lanka (GoSL) can alter domestic law to coerce a certain restructuring arrangement on debt issued under domestic law. Foreign law debt must be handled according to those relevant laws and can be subject to international arbitrations courts.

This breakdown of debt clarifies that regardless of the holder and denomination of the debt, how particular types of debt must be handled in the restructuring process. In Sri Lanka this has a few implications:

The ISBs held by domestic banks also have to be handled alongside the rest of the ISBs – the government cannot negotiate with the domestic banks separately per se, though CBSL can provide specific regulatory forbearance measures for the domestic banks’ exposure to the ISBs.

The dollar denominated SLDBs, and loans must be handled under a domestic debt restructuring process.

The rupee denominated bonds/bills held by non-residents are subject to any restructuring arrangement the government decides to do with regards to those bonds/bills.

Table 3: Public debt by legal jurisdiction at issuance as at end-June 2022, US$ million

Source: Author compilation based on Ministry of Finance data release and Central Bank of Sri Lanka Monthly Bulletin

The key takeaway from this is that the number to use depends on what you want to describe:

Are you looking for Sri Lanka’s public debt outstanding to foreign creditors? Then use residency.

Are you looking for Sri Lanka’s public foreign currency debt burden? Then use denomination.

Are you looking for Sri Lanka’s public debt which will be covered under an external debt restructuring? Then use legal jurisdiction. But keep in mind certain types of debt are typically not restructured, particularly multilateral debt (including IMF) and bilateral currency swaps.

Next I hope to cover the nuances in the Sri Lanka’s overall external debt burden, which goes beyond the public debt to cover the private sector’s debt as well.