What happened to Sri Lanka's Gold Reserves?

Another cost of Sri Lanka's 2018-2022 crisis years

What if I told you that Sri Lanka’s foreign reserves could be higher by close to USD 3 billion now if the central bank still had the same volume of gold it had in 2018? This article is a look at what happened to Sri Lanka’s monetary gold reserves during its crisis years from 2018 to 2022. While I am usually averse to what if analysis, I think of this as a reminder of the costs of Sri Lanka’s deep crisis that otherwise go unnoticed. A cost exacerbated by the record increase in gold prices in recent years.

Others are dipping into their Gold reserves to survive the current crisis

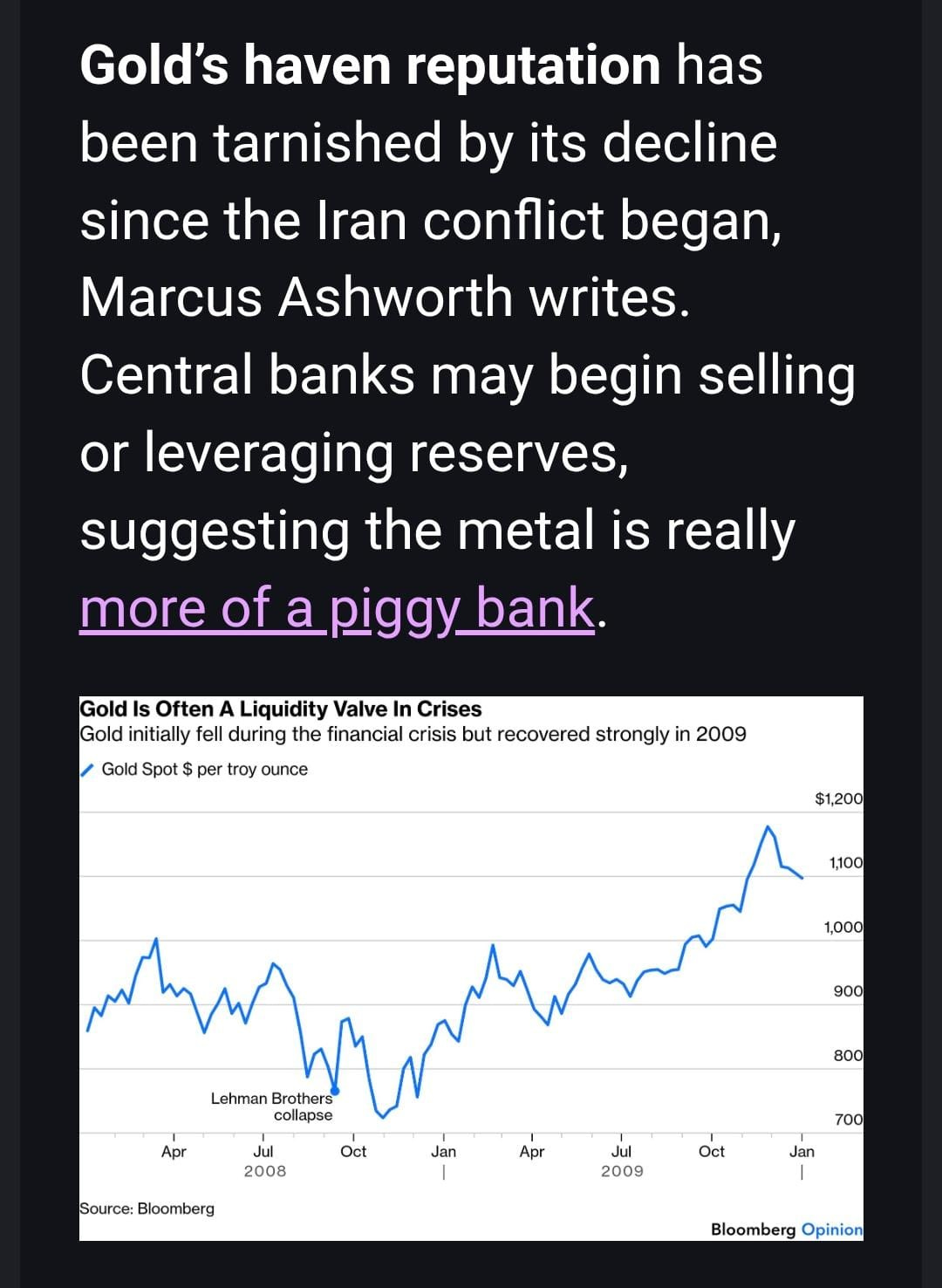

Gold has been the ultimate haven asset over recent years as economic and geopolitical uncertainties have intensified, helping drive gold prices to record highs. So much so, that the reduction in the price since the Iran conflict has been both surprising and substantial.

One explanation given is that some are selling down their gold assets to help pay for the sudden increase in costs from the Iran conflict, especially fuel prices. Central Banks were amongst the largest purchases of gold in the last few years, and now they might be selling some of their gold to help support their currencies and offset impact of their countries’ rising import bills.

But Sri Lanka’s reserves have little in terms of Gold assets

In contrast, Sri Lanka’s central bank has very little in terms of gold assets in its gross official reserves. By February 2026 it was reported to be about USD 200 million, recovering from lows below USD 30 million prior to mid-2023. But that is no where close to the gold assets of over USD 900 million in 2016, 2017/18, and 2019.

But looking at the gold assets in USD terms is not sufficient given changes in the volume of gold and the price of gold affects the value of the gold assets. Even as gold prices rose gradually from 2018 to 2022, Sri Lanka kept selling down its volume of gold. As a result, there was little gold remaining to benefit from the massive rise in gold prices from 2023 onwards. So what happened to Sri Lanka’s gold assets between 2018 and 2022?

Sri Lanka’s Gold reserves prior to 2018

CBSL’s reserves data reports the USD value of gold assets since November 2013 and the volume of gold in millions of troy ounces since June 2015. But I managed to back calculate the estimated volume going back to November 2013 using the market value of gold at the end of each month.

This shows that prior to June 2015 there was more volatility in the volume of gold around the 0.7 million ounces mark (about 22 tons), likely indicating active trading in gold during the period prior to 2015. But from mid-2015 onwards, the volume was much more stable at 0.72 million ounces until the first sale in March 2018.

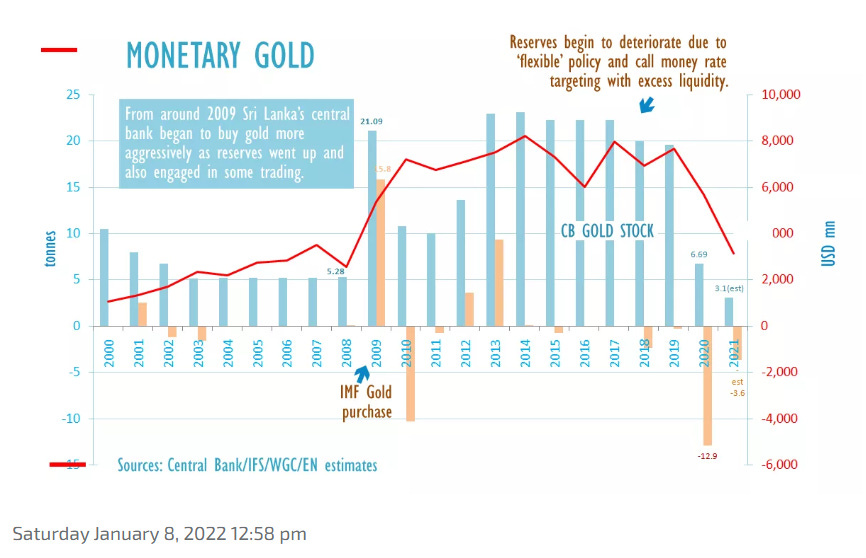

The increase in Gold asset volume to around 22 tons was due to the purchase of 10 tons of gold from the IMF in November 2009 for USD 375 million. This was enabled by the USD 2.6 billion Stand-By Arrangement agreed with the IMF in July 2009, with about USD 660 million disbursed by November 2009. The jump in gross official reserves to over USD 5 billion, driven by a massive jump in foreign investments in rupee government securities, also created space to diversify reserves into more gold. According to data reported by EconomyNext in January 2022, the gold volume reduced during 2010-2012, but rose again in 2013 to above the levels in 2009.

A Series of Gold Sales from 2018 onwards

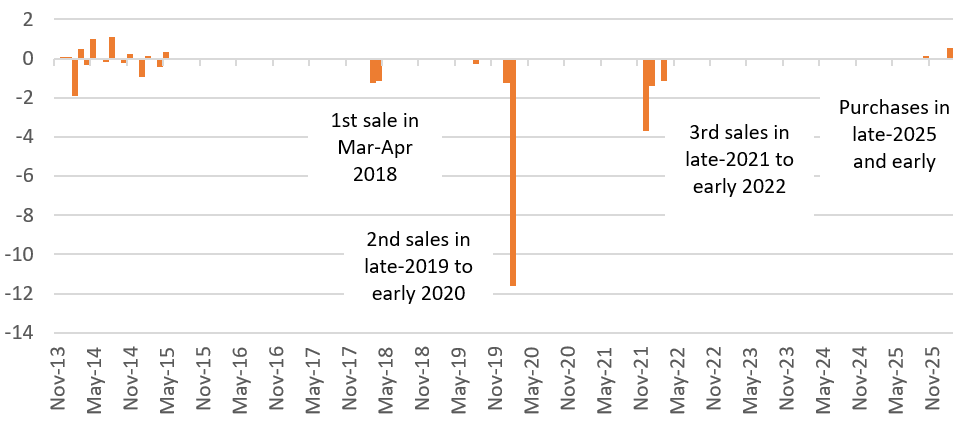

The volume of gold starts to reduce for the first time since mid-2015 in March and April 2018, with a total reduction of 0.08 million troy ounces or about 2.5 tons of gold (roughly 10% of the gold). This was a roughly USD 100 million reduction in gold, but coincided with a USD 2 billion increase in gross reserves, driven by a USD 2.5 billion ISB issuance.

The gold volume remain stable around 0.64 million troy ounces or about 19.9tons of gold until August 2019 when there was a 0.01 million troy ounce or 0.3 ton sale. This was followed by a significant 0.41 million troy ounce or 12.75 ton sale in January and February 2020 that reduced the gold volume by about 66%. This was done just before the COVID-19 pandemic and following the then government’s decision to cut taxes in December 2019. Gold prices rose about 25% across 2020, allowing for the remaining gold to gain in value by USD 67 million.

The remaining 0.22 million troy ounces or 6.8 tons remained until early 2022, when 6.2 tons were sold between December 2021 and March 2022, as the government scurried to utilize all remaining reserves to delay the inevitable sovereign default and pay for essential imports.

The remaining 0.015 million troy ounces or 0.47 tons of gold have remained so until September 2025. Purchases of about 0.16 tons in October 2025 and about 0.56 tons in February , raising the total to over 1 ton.

Sale of Gold assets, tons

What drove these gold sales?

While gold has been a long running reserve asset, it is not a very liquid reserve asset and its price can be volatile at times. A famous case of liquidating gold reserves was India’s 1991 liquidation of Reserve Bank of India’s gold to source foreign currency until an IMF program was negotiated. Some of them had to be airlifted to international financial centers.

Sri Lanka’s case was no different, especially in the run up to the 2022 crisis. Having a billion dollars in gold did not help when there were large regular foreign debt repayments to handle or when there was no foreign currency to pay for shipments of fuel. Even as early as 2018, 2019 and 2020, these liquidity concerns were increasing. But in 2018 and 2019 this was less of a dire concerns due to the ability to raise ISBs, term loans, and the lease proceeds from the Hambantota Port lease.

The reserve management policies of CBSL also changed over time, adapting to the changing context of Sri Lanka’s fiscal and balance of payments situation, and changing global financial conditions. By 2018 the return or yield on US Treasury securities, the ‘safest’ USD asset, was increasing from the record lows in the aftermath of the global financial crisis of 2007/08. As a result, it was relatively more attractive to hold a higher proportion of reserves in USD assets than in gold. Gold in itself has no regular yield or income to the central bank, and might even carry a cost to maintain in secure vaults.

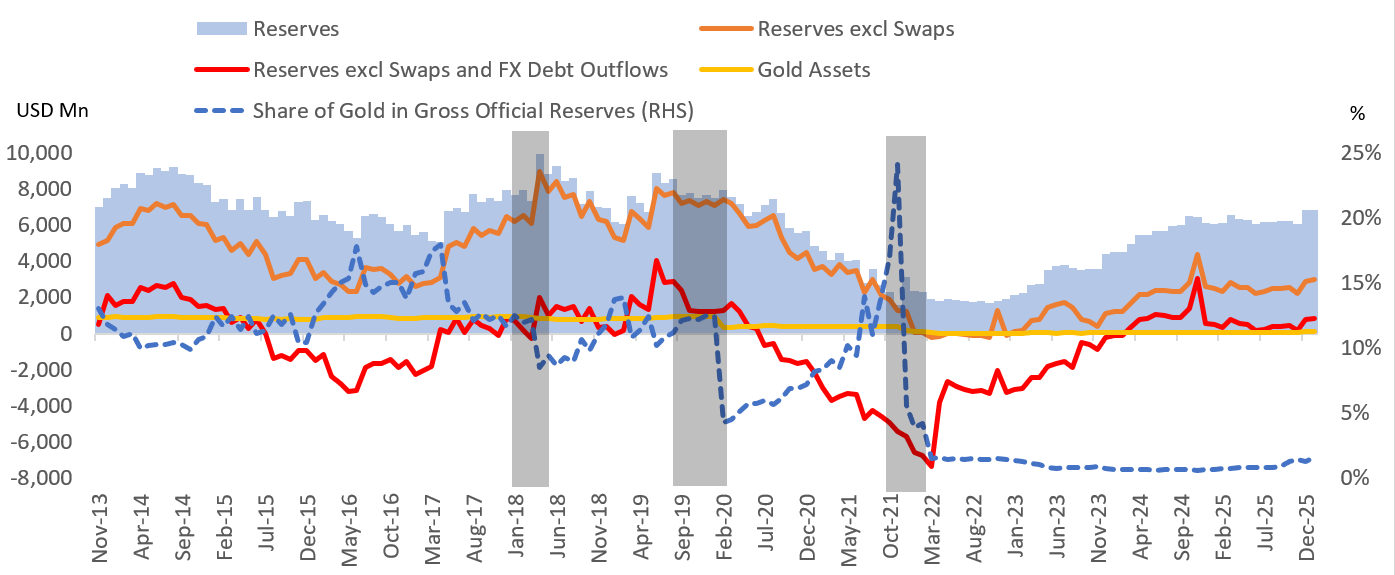

It is easy to look at gold as a share of total reserves. But the actual usable reserves vary over time depending on the amount of swaps and other short term obligations of the central bank. And the illiquid nature of gold can reduce the usability of reserves even further. As a result, the amount of gold assets to be maintained would also need to adjust alongside changes in usable reserves.

CBSL’s explanation of its early 2020 sale of gold was based on these lines, citing the changes to its reserve management policy in 2016.

CBSL policy changes were also taking into account changes to the IMF’s reserve adequacy metrics. In the 2000s, the IMF Article IV consultations and programs focused more on the headline reserve amounts, months of imports coverage, and ratio of reserves to short term external debt. Gold assets in reserves were usually considered in their gross amounts, without accounting for their illiquidity.

But with the introduction of the Assessing Reserve Adequacy (ARA) framework in 2011, the IMF’s approach changed. IMF reports started showing reserves with and without gold, alongside an augmented ARA metric that applied a discount to gold assets to reflect their illiquid and price volatile nature.

Gold amidst Usable Reserves reality

During 2018, 2019, and early 2020, gross reserves were at relatively high levels, staying above USD 6-7 billion. But when adjusted for swaps and FX debt repayments due in the next 12 months, ‘usable’ or remaining reserves were much lower. Selling some gold to increase liquidity of the remaining reserves made since in such a context.

Gross Official Reserves adjusted for Swaps and FX debt outflows in 12-month forward pre-determined FX drains data

By late-2021, the price of gold had increase boosting the value of the remaining gold and the decline in reserves had increased the share of gold in reserves to above 15%. With the then government insistent on paying the USD 500 million ISB maturing in January 2022 and FX being desperately needed to pay for fuel shipments, liquidating the remaining gold would have been a no brainer. No central banker can refuse to liquidate some gold when payments for essential goods were at stake.

There was no law that prevented or limited such sales. The then government’s insistence of using up all possible space to avoid default till the last possible minute meant there was no option for the central bank.

The What if Scenarios

So, what if Sri Lanka still had the gold that was available prior to each major sale of gold assets from 2018 onwards?

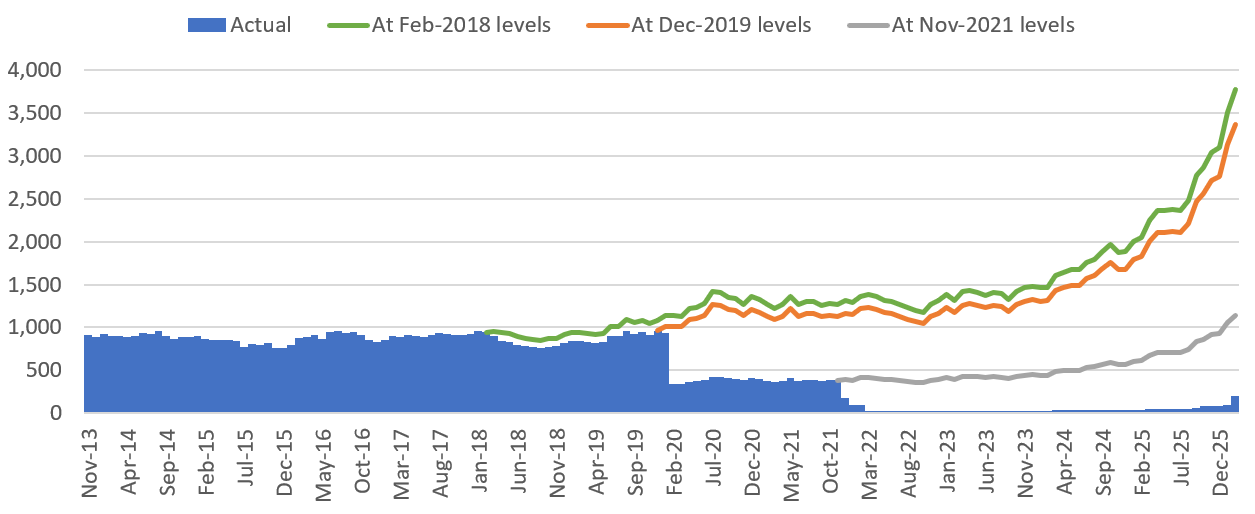

Compared to the USD 200 million in gold at February 2026, retaining the volume of gold in 2018 and 2019 would have allowed for USD 3.3 to 3.8 billion in gold assets, driven by the massive increase in gold price.

But even if the gold assets remaining in November 2021 were retained, instead of paying the USD 500 million ISB in January 2022, the gold remaining would have been about USD 1.1 billion.

Actual vs. Hypothetical Gold Reserve Assets, USD million

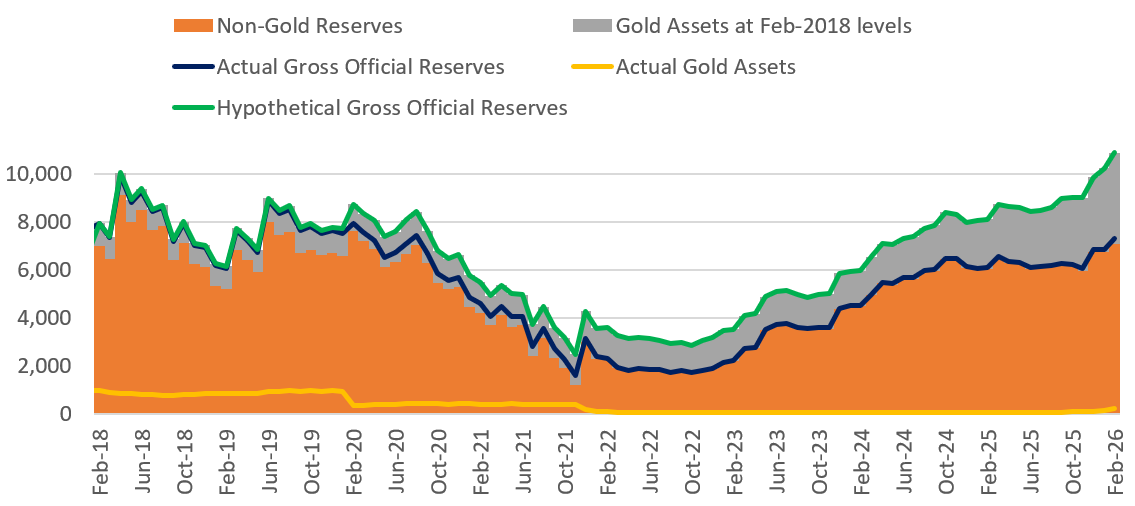

At the Feb-2018 level of gold, the gross reserves would currently by about USD 3.6 billion higher by now.

Gross Official Reserves Actual vs. Hypothetical at Feb-2018 Gold asset levels, USD million

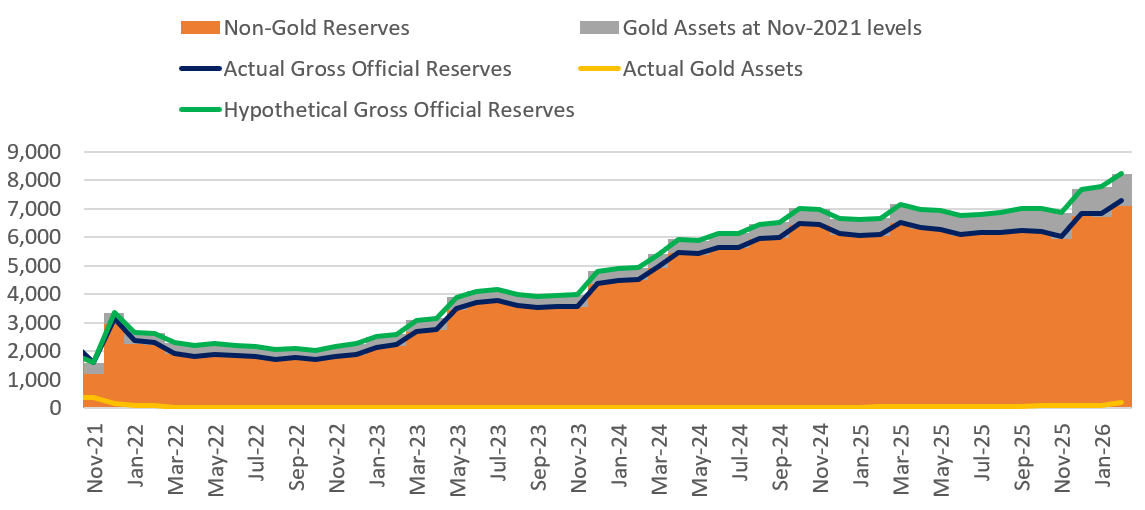

At the Nov-2021 level of gold, the gross reserves would currently by about USD 1 billion higher by now.

Gross Official Reserves Actual vs. Hypothetical at Nov-2021 Gold asset levels, USD million

Of course these are hypothetical what ifs, meant to illustrate the cost of the 2018-2022 crisis period in which desperate measures were taken to keep muddling through amidst multiple shocks. Reality is more complex. Priorities of central bank reserve management goes beyond holding large gold assets in hopes of a massive rally in gold prices. Immediate near term concerns take precedence. Which is why it is important that the political decision makers need to manage risks holistically and avoid seeing reserves as providing money and time they can use for policy gambles.

Note: This article is based on the personal analysis and opinions of the author. It is in no way a reflection of institutions that the author is affiliated with. Any errors or omissions are the author’s sole responsibility.

To become the Switzerland of South Asia we need to start building a voracious appetite for Gold. Buy as much of it as humanly possible by depreciating the currency.